Policy Turnaround

China's fintech industry faces new

regulatory headwinds

China's fintech industry is booming. 74% of Chinese consumers make daily payments by smartphone, and more than 40% (605 million) of Chinese citizens did not go to a traditional bank in 2020 but used online services to invest their money. And the InsurTech market has also been growing since 2015 with growth rates around 15%.

The market is dominated by innovative technology companies. Traditional financial service providers such as banks have not yet played a leading role. First and foremost is Alibaba's financial arm, Ant Group, which has long since not only operated the mobile payment service Alipay, but now generates half of its revenue from other financial services such as microloans, the money market fund Yu'e Bao, and online insurance. Other major players are Lufax, a subsidiary of Pingan Insurance and specialized in wealth management and personal loans, or ZhongAn Finance in the field of online insurance.

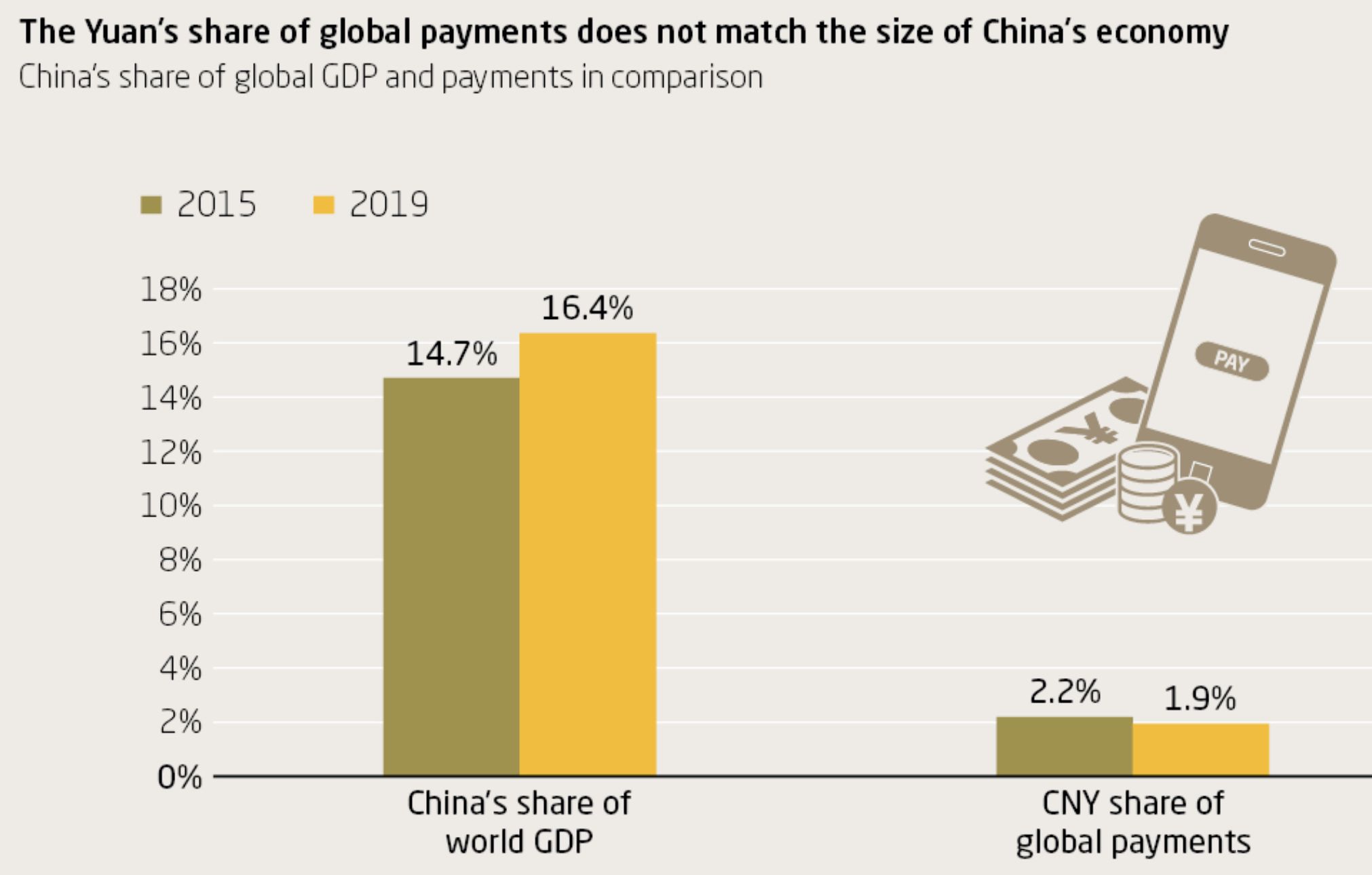

China's fintech companies have so far focused heavily on the domestic market, and international expansion plans are more likely to be directed to Southeast Asia than to Europe for the time being.

Graph: Merics

Graph: Merics

Only in the area of mobile payment services are there exceptions. For example, Ant Group acquired minority shares in the European payment service provider Klarna. And especially in luxury stores and in retail at international airports, payment via WeChat Pay or Alipay is also possible in Europe. Here, the companies are following Chinese tourists and expats who do not want to do without their convenient payment methods abroad.

The rapid growth of the fintech industry has been made possible by several factors: China's previously relatively underdeveloped financial system, a great curiosity and willingness among Chinese consumers to use new technologies, the availability of data, and finally, above all, a relatively unregulated market - the latter is now changing.

The duopoly of Alipay and WeChat Pay is increasingly a thorn in the side of the Chinese government. With 55.6% and 38.8% each, they dominate mobile payments in China.

The duopoly of Alipay and WeChat Pay is increasingly a thorn in the side of the Chinese government. With 55.6% and 38.8% each, they dominate mobile payments in China.

China's digital economy as a growth engine

in mn RMB and in % of GNP

Guo Shuqing, China Banking and Insurance Regulatory Commission (Bild: Keystone)

Guo Shuqing, China Banking and Insurance Regulatory Commission (Bild: Keystone)

While the Fintech Development Plan published by China's central bank in 2019 still spoke of "fintech as a new engine for high-quality financial development" and "a new weapon to prevent financial risks," the industry's own systemic financial risks are now coming into focus. For example, Pan Gongsheng, vice governor of China's central bank warned in January 2021 that "the cross-border, cross-industry and cross-regional nature of the [fintech] sector means that financial risks are spreading faster and further with greater spillover effect." In March 2021, State President Xi Jinping used unusually strong words to call for a crackdown on Internet-based platform companies. Among other things, he called for regulators to fight monopolies, promote fair competition and prevent the disorderly expansion of capital, and for any financial activities to also be covered by financial supervision.

Increased competition in the mobile payment sector

The duopoly of Alipay and WeChat Pay is increasingly a thorn in the side of the Chinese government. With 55.6% and 38.8% each, they dominate mobile payments in China. They know how to leverage this power: Ant just announced to increase fees for retailers.

The Chinese government is responding accordingly: a January 2021 draft of the "Regulation of Non-Bank Payment Service Providers" stipulates that no mobile payment provider may have more than one-third or two payment providers may have more than half of the market share - but both apply to WeChat Pay and Alipay.

The introduction of the digital currency by the Chinese central bank can also be seen in this context. The digital currency is designed as a retail currency and is recognized as legal tender. This means that every retailer must accept payments with the digital currency. The fact that the payments also work without the Internet and that there are no fees for subsequently retrieving the cash from the mobile payment service provider makes the digital currency attractive to retailers. The two-stage model, with the central bank issuing the digital currency first to financial intermediaries and then to end users, means that other electronic wallet providers are entering the market as competitors to AliPay and WeChat Pay. The technology group Huawei, for example, is already in the starting blocks and acquired a payment license at the end of March 2021. In addition, the pilot projects for the digital currency are progressing rapidly - the Winter Olympics in Beijing in February 2022 could be a possible starting point for nationwide introduction.

Two-Stage model of the chinese digital currency

Chinese central bank deals with intermediaries

The intermediaries distribute the digital currency to individuals and companies

Systemic regulation across the fintech sector

However, the Chinese government is not only focusing on mobile payment service providers, but is also pushing ahead with a whole range of measures that affect the entire fintech industry. The main focus here is on containing systemic risks and reducing regulatory arbitrage opportunities.

Due to the lack of regulation, the leading fintech platforms in online lending, for example, outsource a large part of their risks to the banks. While the platforms guarantee billions of dollars in consumer loans, only a single-digit percentage of these loans appear on their own balance sheets (at Ant Group it was 2% of a total volume of 1.7 trillion RMB), while the rest is financed by banks or asset-backed securities.

The Chinese government is responding to this with so-called 'function- and behavior-based supervision'. In the future, it is not the type of company, i.e. whether it is a financial or technology company, that will determine which regulations take effect, but the actual company activity. As a first measure, fintech companies that make joint online loans with commercial banks must now contribute 30% of the loan amount.

The required restructuring of fintech companies into so-called financial holding companies will be particularly disruptive. Restructuring is required when a company is active in two or more financial businesses and its total assets reach a certain threshold. As financial holding companies, the companies will then be regulated similarly to banks with significantly higher capital requirements. This will visibly slow down the previously rapid growth. The first company to be affected by this measure is Ant Group, where, according to media reports, a joint decision on the exact form of the restructuring has already been reached with the supervisory authorities. However, a look at the structures of China's fintech players shows that far more companies will be affected: Tencent, Baidu, Jingdong, Suning and Xiaomi's financial platforms are also involved in various financial activities, such as mobile payments, consumer loans, corporate loans, wealth management or insurance.

Stricter rules for data protection

In addition, fintech companies' data-based business models face increasing restrictions. A new proposal to regulate the use of credit score data restricts excessive data collection and increases personal privacy protections.

A research paper from the Chinese central bank also calls for data from digital platforms to be defined as a public good and regulated accordingly. In addition, there is a report on a possible plan by the Chinese central bank to set up a joint venture together with Internet companies to centralize and monitor collected data in a separate structure.

Exactly which types of data and which sources are to be possibly transferred to the management of the joint venture here is still unclear. Even if these measures have not yet been decided, a trend is emerging: the availability and free use of data, until now one of the decisive advantages in the Chinese fintech market, will decrease.